Emergency Fund

Your Financial Lifeboat - Build It Before You Need It

TL;DR

Emergency fund takes the sting out of the costs of an emergency (although it still hurts!)

Aim for 3-6 months of livings costs if employed, 6-12 months if self-employed

Target is between £10k-£20k for most people

Keep emergency fund in an easy access savings account

Why It Matters

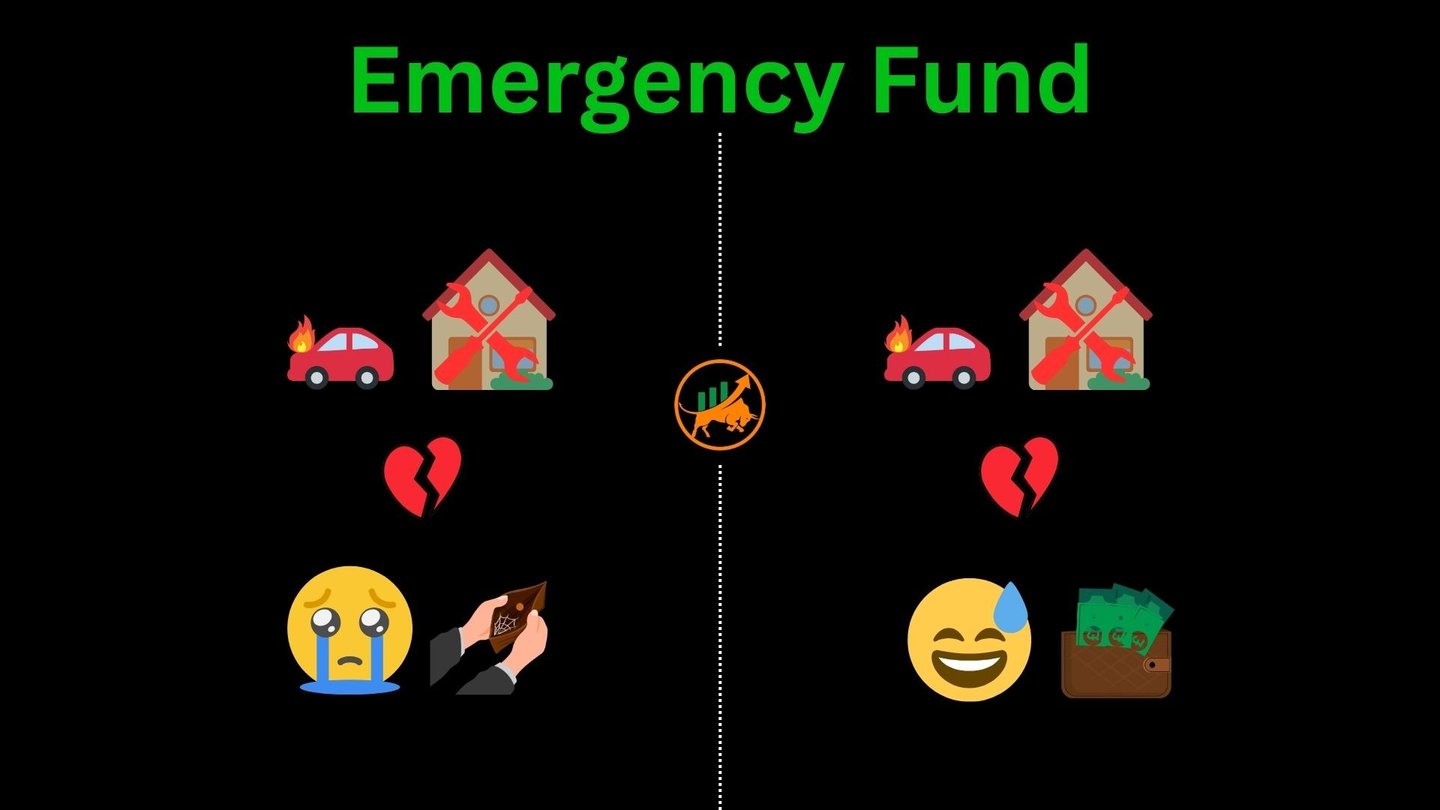

Life happens (or sh*t happens) and you need to be financially prepared for it.

A job loss, broken boiler, car repair, maybe even a medical bill that isn't covered by NHS or your insurance.

Without an emergency fund, you risk going into debt or be forced to sell investments to cover the cost of the emergency. Neither of these are appealing and add stress to an already stressful situation.

On the other hand, with an emergency fund, yes, it still stings and it's still stressful, but, you're calmer, more in control, have more time to think and do not have to stress about where the money is going to come from because you have it readily available.

Feel a little better? Good!

How Much?

To start, build a baby emergency fund of £1,000. It's small enough to not feel daunting but big enough to cover most inconveniences. Then go from there. Every £ counts!

Calculate your monthly living costs using the tracker tool to get your own number and use the general guide below:

Single, no kids, renting: 3 months

Family, mortgage, employed: 6 months

Self-employed, variable income: 6-12 months

Where To Keep It?

Keep your emergency fund in a completely separate easy-access savings account. This will prevent the temptation to spend it on non-emergencies.

The best place to find the top paying interest rates on easy-access savings accounts is Money Saving Expert, who regularly update their list.

You can also keep it in a cash ISA, which is easy access with the added advantage of any interest you earn being tax free, although the interest rates are typically lower than easy-access.

Do not keep your emergency fund in stocks, pensions or fixed-term savings account as these are for long term wealth building and are either inaccessible, penalise you for withdrawing or fluctuate in value. Not great if you need the money fast!

Common Mistakes To Avoid

Don't redefine an emergency to satisfy a luxury spend such as a holiday or new phone! It may be tempting but these items should be saved for in a separate savings goal, far away from your emergency fund.

Don't keep it in a current account that is paying 0% interest. You want to build your emergency fund so why not make the most of interest paying savings accounts to help get you to your target faster?

Don't give up after £100 because momentum matters with everything. Keep going and celebrate the small steps along the way towards the big win. Your future self will thank you massively.

After An Emergency

Firstly, we hope that it all turns out ok but once the emergency is over, then focus on rebuilding the emergency fund back up again so you're covered for next time.

Take Action

Now you know the importance of an emergency fund and how it is best used, here's your homework:

Calculate your monthly essential costs

Multiply by 3 to get your starter target

Set up an easy access savings account and start auto-transferring what you can to start building

Be emergency ready. You've got this!

Are you ready to start building yours?