Debit vs Credit

The Two Cards and Concepts That Shape Your Debt

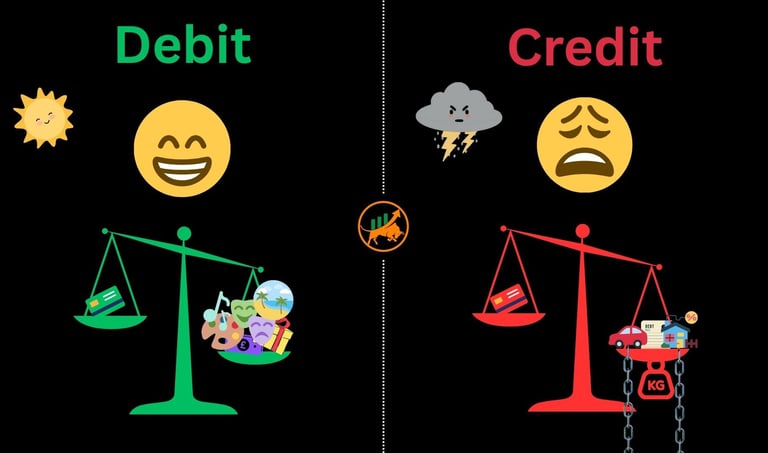

TL;DR Debit vs Credit In A Nutshell

Debit is your own money, not someone else's = no debt

Overdrafts bail you out of real emergencies but should generally be avoided

Credit is borrowing someone else's money that you must pay back with interest = debt

Use credit carefully to avoid the interest trap

The Debit Approach

For the debit approach, you would follow your SMART goal diligently to save up the required amount of money over time to buy the thing that you wanted.

Whatever amount is on your bank debit card is your own cash, no-one else's, which is good news. You don't owe anyone anything. Perfect.

Debit accounts typically don't pay interest like a savings account does so they are mainly used for spending as opposed to saving.

However, there may be some debit cards that offer cashback incentives or other rewards so make sure you understand the terms and conditions before switching accounts.

Any transaction you make with a debit card is completed instantly but you can only spend the amount you have on your debit card, unless you have an overdraft.

The Hidden Trap of Overdrafts

An overdraft is a feature of your debit card that comes in to effect when you spend more than the money available on your debit account.

This effectively turns it into a short term credit card with the only real benefit being to bail you out of a real emergency.

Generally, overdrafts should be avoided as you have to pay back the extra amount owed, with a lot of interest and it defeats the point of having a debit card. Overdrafts fall in to two categories:

Arranged - you have a pre-arranged limit with the bank that you can borrow after you have overspent your debited amount

Unarranged - you have no pre-arranged limit or exceeded the pre-arranged limit

Neither of these are an ideal solution and if you find yourself frequently going into overdrafts, it has negative consequences on your credit score and you'll pay more back with interest, hampering your ability to gain financial strength.

Therefore, keeping a decent enough buffer on your debit card can mitigate the risk of going into an overdraft unnecessarily.

The Credit Card Disguise

Credit cards are a loan in disguise where you borrow money from the bank and pay them back.

The bad part comes when you don't pay the balance back (i.e. how much you borrowed) in full each month as you get hit with a very high interest rate, typically 20%+.

By not paying back your balance, even for one month, your credit score will be negatively impacted, which will affect your ability to borrow more in the future (e.g. for a mortgage).

The further downside to this is that money that you could have put towards your savings goals now has to be redirected to paying off interest on a debt that you don't want instead.

Future you is not happy about this.

Credit Cards Done Right

So are there any positives to credit cards? Yes, but only when you do it right.

By paying the balance back in full each month, this means you have zero interest, zero charges and a positive impact on your credit score.

An excellent credit score means you have proven yourself to be trustworthy with money and paying off credit. Mortgage lenders have a keen eye on credit scores and will be more likely to lend to you, potentially giving you a favourable interest rate, that you may not have otherwise got with a not-so-good credit score.

Some credit cards come with benefits such as points that can be redeemed for vouchers or air miles, which can help contribute to your SMART goals.

Again, you must make sure you pay off the balance in full each month, otherwise you risk losing the benefits, as well as the other negative effects mentioned before

One final point about credit cards is that they legally come with buyer protection for items over £100 (and less than £30k). This means that your credit card provider is jointly responsible with the retailer if something goes wrong with your purchase - tip: check Section 75 of the Consumer Credit Act.

Debt Escape Plan

If you have found yourself in credit card debt, then escaping from it is of paramount importance to get you back on track. We want you to succeed with money so that you can enjoy life as much as you can and being in debt is not fun.

There are two approaches commonly used to overcome debt:

Debt Snowball - attack the smallest debt first, minimum payments on the rest until paid off, then attack the next biggest and so on

Debt Avalanche - attack the highest interest debt first, minimum payments on the rest until paid off, then attack the next highest interest rate and so on.

The Snowball approach is good to build initial momentum and see a quick win. The Avalanche approach is good to pay less in interest and have more money at the end of it all.

Either way, both approaches give you the chance to pay off your debt and release yourself from the chains that are stopping you from nailing your finance goals.

Action Points

Your homework is as follows:

Track your spending via the Track & Win Spreadsheet and understand where your £ are going

Check your latest credit card statement and pay the balance in full

If in debt, freeze any spending unless necessary and create SMART goal based on Debt Snowball or Debt Avalanche approach.

You've got this!