Assets vs Liabilities

What Builds Wealth and What Drains It

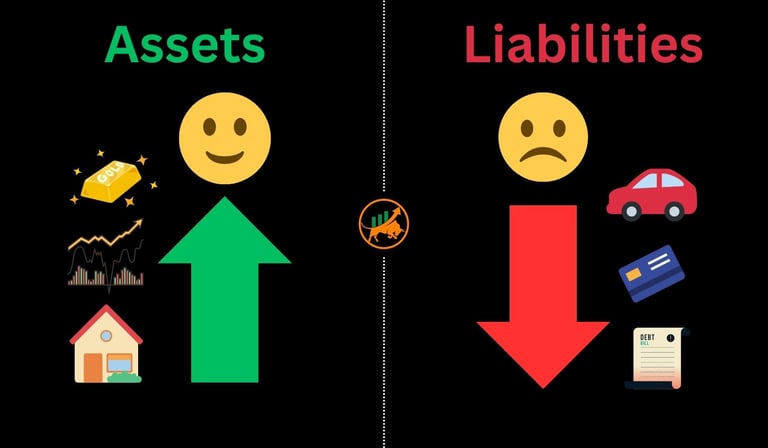

TL; DR - Assets & Liabilities In A Nutshell

Assets put money in to your account

Liabilities take money out

Your goal is to have more assets and less liabilities

Cash-Flow Is The Secret Sauce

Cash-flow is your greatest ally but it can also be your greatest foe. If your cash is flowing out into liabilities, then you will not be able to build your financial strength to reach your goals.

However, if you can get your cash flowing into assets that can help generate cash-flow into your account then you can start to build real financial strength.

Robert Kiyosaki, well known in the finance world for his book "Rich Dad, Poor Dad", often mentions that:

Rich people buy assets first

Poor people buy liabilities first

Middle class people buy liabilities that they think are assets

Liabilities

We need to understand what is regularly taking money from you each month so let's start with liabilities first, which typically include, but are not limited to:

Mortgage/Rent of the house you live in

Car loan payments

The car itself as they generally go down in value

Student Loan payments

Credit Card debt repayments

Any other loans (personal, payday etc.)

Interest on loans

Insurance (car, home, pet)

Monthly bills (gas, electric, phone, internet, water)

Tax (car, council, capital gains, VAT, NI, income)

Subscriptions that you don't use

As you can see, liabilities can add up quickly and having too many liabilities means you're forever paying money to people or companies, making them richer instead of you.

Remember, the borrower is a slave to the lender.

So it is in your best interest to minimise liabilities where possible so that you can have more financial attention on things that put money into your account.

Assets

Apart from you being your greatest asset (so cliché!), you have a few financial instruments that you can use to help put more money into your account and grow your net worth. Some examples are below (and this is not to be considered financial advice):

Stocks & Shares

Dividends & Exchange Traded Funds

Real Estate (rent money from tenants, selling your own residential property for a profit)

Interest bearing accounts (savings, General Investment Accounts)

Bonds & Mutual Funds

Digital assets (although it needs to be stressed that you should be prepared to lose all your money with digital assets)

Your own business that sells products/services (side hustle included)

Pensions

Commodities (oil, gold, silver)

The important point to be wary of is that the underlying value of these assets can also go down so understanding your own risk tolerance, managing that risk and having a well-researched and informed approach to investing will put you in good stead.

Having said that, if you can eliminate some liabilities, you will have given yourself an immediate pay rise, which is not to be sniffed at!

Your 3-Step Audit

Now that you have an idea of what assets and liabilities are, it's time for your homework and for you to do your own asset vs liability audit:

List out everything you own*

Ask yourself: "Does this put £ in my account?"

Create a SMART goal to eliminate one liability and acquire one asset in its place.

*put assets in one column, liabilities in the other. This is called a "balance sheet"

Start this tonight and finish the SMART goal this week - see how your mindset starts to shift towards acquiring assets.

You've got this!